The water and wastewater industry is in transition to a digital revolution that has the potential to transform the industry from the use of data-driven technologies, with utility sector spending dwarfing the industrial market. This is according to a new report by Global Water Intelligence (GWI) that provides a detailed guide to the opportunities in this smart market.

The global market for control and monitoring systems in the water sector is estimated to be worth $21.3 billion in 2016, growing to $30.1 billion in 2021. Spending on advanced data management and analysis solutions is expected to grow even faster, at 11.9 per cent a year. In the utility sector, spending on digital and smart solutions is estimated to be worth $17.7 billion in 2016.

Managing water relies on heavy physical infrastructure and inherently reactive governing attitudes. This is changing with the development of cyber-physical systems, real-time monitoring, big data analysis and machine learning with advanced control systems and the Internet of Things (IoT). These “smarter” systems; in which technology, components, and devices talk to each other and feed information to each other in a more sophisticated way bring about a more optimised, efficient process.

“Utilities and industrial water users are beginning to understand that there is a big picture here beyond this mosaic of different suppliers. It is a vision of the digital utility which brings together all the different parts of this world of data collection, processing and automation which promises to deliver significant efficiencies with a high return on investment.” Christopher Gasson, publisher, commented, “The next big consolidation in the water sector is going to involve monitoring, control and data management.”

Water’s Digital Future outlines the major opportunities available to players in the different layers of monitoring and control systems. It shows the gaps in the market, what is motivating the end user to invest in a solution and how the solution provider can access the market.

According to the report, the utility sector is the largest part of the market with numerous opportunities for utilities to save money using smart technologies to improve asset management, process optimisation and interaction with their customers. Whilst in the smaller industrial sector, process efficiency and product quality are the main factors driving greater adoption of these smart technologies.

In the utility sector, there is a huge opportunity for increasingly sophisticated data analysis as utilities understand the benefits of viewing their networks and assets in a catchment-to-tap way. This is driving spending on sensors and customer metering to obtain greater amounts of data about network and treatment process, and external data such as weather and geological information. More advanced data software solutions are needed in order to integrate these increasingly diverse sources.

Within the Industrial market spending across all industries is expected to increase over the forecast period 2016-2021. Industries such as microelectronics are market leaders with advanced solutions while others such as food & beverage lag behind. The most interesting opportunities in the industrial market include; upstream oil and gas, refining and petrochemicals, power generation, mining, food & beverage, pulp and paper, pharmaceuticals and microelectronics.

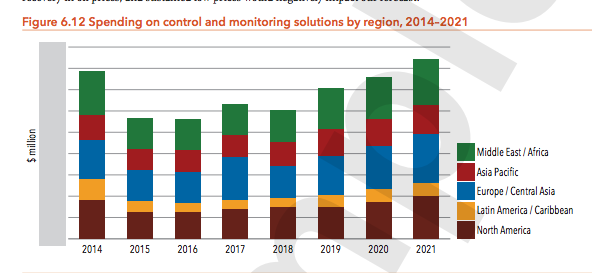

The report reveals that the biggest market for smarter control and monitoring systems is Asia Pacific where spending is expected to reach $10.3 billion in 2021, driven by growing urban populations placing pressure on infrastructure. There is a big focus on leakage management in Japan and NRW reduction programmes in Malaysia and the Philippines. Leakage management is also a major role in North America and Europe due to ageing infrastructure within networks and treatment plants that continue to cause problems for utilities.

View the report page complete with table of contents and download a free sample chapter at: www.globalwaterintel.com/watersdigitalfuture

This article talks about the fast growth of the global market for water control and monitoring systems. It focuses on the move to digital technology and the great chances for saving money and improving efficiency in utilities. Thanks for sharing this important information!