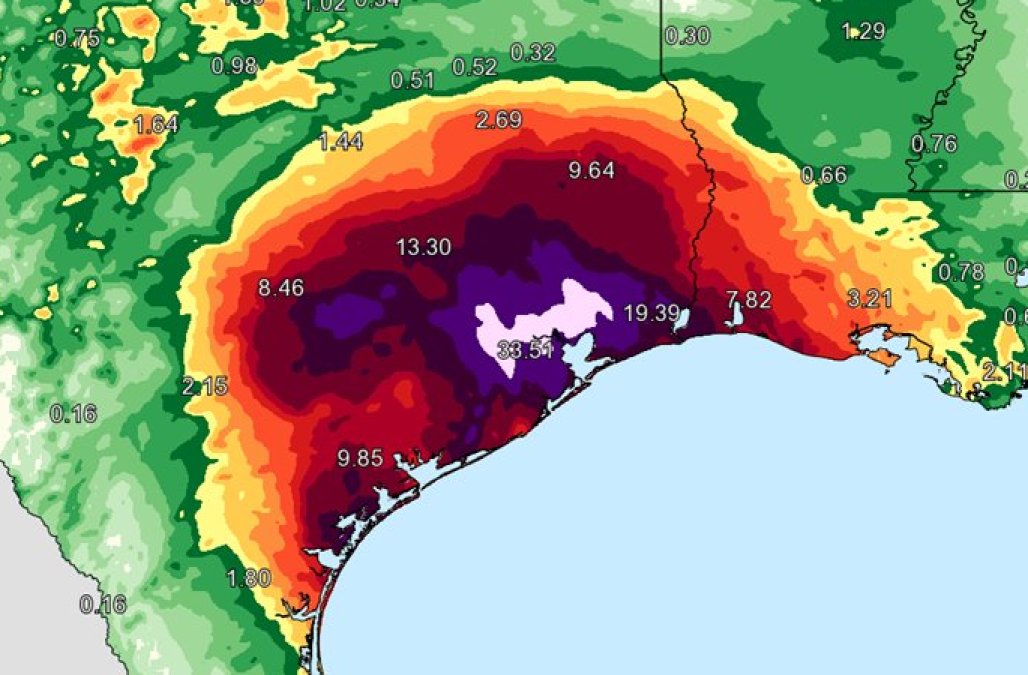

Every decade or so there is a global catastrophe that redefines the conversation about public policy. For those interested in coastal development and climate change, Houston, Texas and Hurricane Harvey is that event. An estimated 127 centimetres of rain has fallen on the Greater Houston Area—so much rain that the National Weather Service had to update the colours used to map the rainfall.

For those on the outside, it is difficult to comprehend the challenge ahead. The damage, by some estimates, will range between $10–30 billion. To make matters much worse, the Federal Flood Insurance Program is already about $20 billion in debt due to Hurricanes Sandy and Katrina, and Tropical Storm Irene; and the Federal Flood Insurance Program is set to expire on September 30th—when the U.S. Treasury Department will hit its debt limit. Oy vey! But lets assume for one minute that the funds to rebuild will surface somehow. There are lessons to be gleaned from Harvey.

Dr. Charles Colgan is the director of research at the Center for the Blue Economy (CBE). He has served the National Ocean Economics Program (NOEP) as a consultant for more than 14 years, and he is the lead author of a new study prepared for Lloyd’s of London that examines options for financing natural infrastructure that helps protect against future flooding and storm surges. Colgan also believes that there is plenty of funding out there for natural infrastructure projects.

I think that if you look at Harvey or any of these storms, and you say ‘haaa, well now is the time that we’ll make massive investments in resilience;’ I would say, ‘Well no, that’s not going to happen, because recovery still comes first,’” said Colgan. “But there are smart ways to recover and dumb ways to recover. There are ways that you can build resilience over time.”

Colgan and his co-authors noted that in many cases investment to conserve natural habitats makes economic sense for investors and insurers, because natural barriers are less expensive than seawalls for areas in dealing with sea level rise in conjunction with intensifying storms and flooding.

“Over the next 60 to 70 years, we are going to transform those hypothetical [storms] into actual ones, so a phased resilience strategy makes a lot of sense. You don’t want to overbuild and commit resources to floods that might never occur, but you also don’t want to underdo it either. It’s a strategy that’s going to have to play out over decades not in recovery from one storm.”

Innovative finance needed

Colgan et al.’s report states that securing funding to develop and implement resilience strategies will require bold action from industry, government, scientists, and communities. “Nobody has enough money to fix all the problems,” he said.

He believes that the future of infrastructure finance, particularly in the creation of resilient infrastructure, will depend on new financing mechanisms that combine public and private, and even non-governmental funds. Green bonds, the do-good debt, is one financial tool that the authors examine to get the job done, in addition to catastrophe bonds and resilience bonds.

Green bonds help investors fulfill their fixed income investment objectives and, at the same time, make a positive impact on the environment. “The institutional structure that deals with infrastructure has historically not been set up to do that,” said Colgan. “Historically, the departments or ministries of transportation get a share of tax revenue and then spend it or they issue a bond (that is a share of tax revenue) and they spend it. That is infrastructure finance. It’s not going to be enough.”

Globally, green bonds have grown so big in recent years that VanEck rolled out the first-ever U.S.-listed green bond exchange traded funds (ETF) on the NYSE Arca exchange in March 2017. The Organisation for Economic Co-operation and Development (OECD) reported in June 2015 that that the green bond market had a total value of $600 billion.

Catastrophe bonds (also known as cat bonds) and resilience bonds are risk-linked securities that transfer a specified set of risks from a sponsor to investors. They were created and first used in the mid-1990s in the aftermath of Hurricane Andrew, emerging from the need of insurance companies to alleviate some of the risks they would face if a major catastrophe occurred. Insurance companies typically issue these bonds through an investment bank, which sells to investors. In places where there is a foundation of risk assessment and information available on green infrastructure risk management, such funds may be appropriate to finance resilience projects.

Infrastructure banks are also important funding mechanisms because as Colgan et al. note, the banks are ideal for leveraging different resources to fund projects, making them attractive to private capital markets. Given that Canada is in the process of developing its own federal infrastructure bank, Colgan said there is a great opportunity for Canada to build a bank that can capture the benefits of risk reduction in ways that support market-based finance.

“P3 is just the start of this,” Colgan said. “Our focus on the financing of natural infrastructure for flood control purposes doesn’t really lend itself to P3 in a lot of cases, but it’s entirely reasonable to back catastrophe bonds or other kinds of financial instruments by setting up special purpose tax districts.” He added that areas where flood, sewer, water, or stormwater infrastructure is needed at a scale that would generate a large flow of funds, there is great potential to find private investors who will provide the money.

A key conclusion of the report is that the largest opportunities for funding are in the redirection of post-disaster recovery funds to pre-disaster investments in risk reduction. “It will be very interesting to see what will happen with regards to Harvey. I think about half of the Texas Congressional delegation voted against the Sandy recovery project including virtually all the representatives and senators that represent the flooded areas. One of the things they objected to was that all of this extra money was going to ‘stuff that wasn’t needed,’” said Colgan. “What will the package that Congress puts together to deal with Harvey look like?”

Grey infrastructure bias

One of the biggest hurdles for creating more resilient coastlines is overcoming what is referred to as grey infrastructure bias. “There’s a tendency not to do new things because you want to get things done quickly. You might go in with a green infrastructure project and say, ‘Let’s rebuild this wetland or move development of this wetland so that it provides flood control for the next time,’ But there’s nothing in the regulations to help the agencies deal with this stuff. […] There’s a bureaucratic bias against doing innovative things in the recovery process.”

To address this challenge, Colgan explained that environmental and infrastructure agencies need to build in ways of expediting these decisions and enable the flexibility necessary for innovation. “This bias is a fixable problem,” and we must get past the notion that we are aiming to restore what was previously there after a disaster occurs, he added. “Spend as much time and money as you can to improve the situation for next time, because there will be a next time.”

Still, he remains optimistic about the opportunities available. “Most of the people I talk to in the finance field say that there is so much money sloshing around the world looking for places to invest. The innovative approaches in climate bonds and green bonds are a real opportunity for them.”

His suggestion is for governments to identify these opportunities proactively before there is a need. “That’s the lesson: don’t waste a crisis. Now’s the time to go in and put more money than you need to recover into fixing things so that next time it’s not as bad.”

The report entitled, Financing Natural Infrastructure for Coastal Flood Damage Reduction, was developed in collaboration with the Nature Conservancy and UC Santa Cruz. It is available online at http://centerfortheblueeconomy.org/green-financing.